If you didn t deduct enough or deducted too much in any year see depreciation under decreases to basis in pub.

Roof depreciation rate.

You must also take into account the month the roof is installed for the first year.

Divide the yearly depreciation of 545 46 by 4 5.

For example if you install a new roof in august you can claim four and a half months of depreciation for the first year.

Replacementsof the entire roofand all the gutters and all windows and doors of your residential rental property.

Slate tile and metal roofs would have their own depreciation schedules.

Life expectancy of building components will vary depending on a range of environmental conditions quality of materials quality of installation design use and maintenance.

The irs designates a useful life of 27 5 years so divide the total cost of the roof by 27 5 to reach the amount you are able to deduct each year.

For instance a brand new composition shingle roof may depreciate at a published rate of 2 to 3 per year until it reaches a certain minimum amount say 25.

Calculating depreciation begins with two factors.

Improvements are depreciated using the straight line method which means that you must deduct the same amount every year over the useful life of the roof.

Are generally restorations to your building property because they re replacements of major components or substantial structural parts of the building structure.

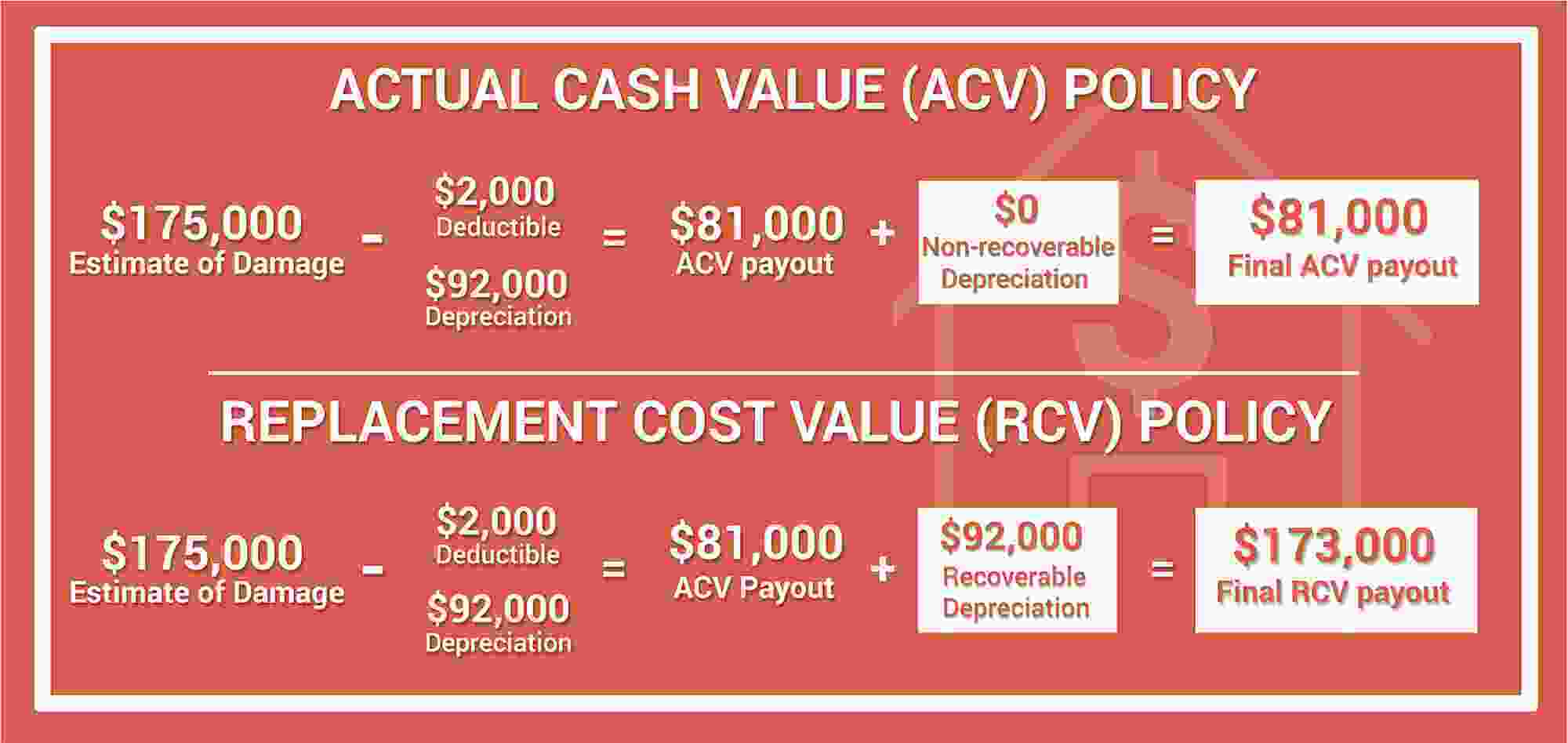

For example if your roof is 25 000 new and is 15 years old on the date of a claim and the insurance company attributes a rate depreciation of 1000 per year on the roof then they will subtract the depreciation from the value of the new roof and only pay you the depreciated value.

The irs uses the straight line method to calculate the depreciation of your roof which means that the depreciation of your roof is calculated evenly across a set period of time.

Special depreciation allowance or a section 179 deduction claimed on qualified property.

15 000 cost of repairs to roof.

An item that is still in use and functional for its intended purpose should not be depreciated beyond 90.

Manufacturers repairers builders and home inspector associations and insurers.

1 000 year depreciation not applicable for rcv.

This means the roof depreciates 545 46 every year.

Cost of repairs to roof.

The information provided herein was obtained and averaged from a variety of sources including but not limited to.